×

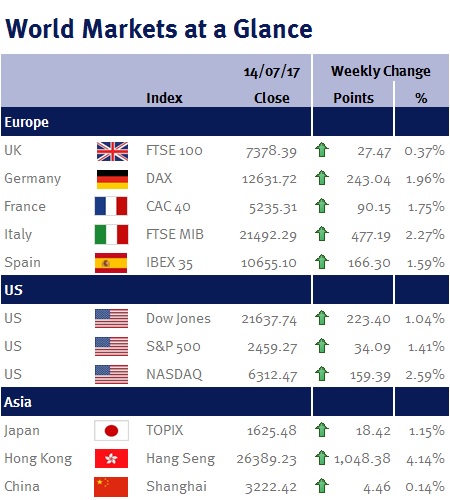

Week ending 14th July 2017.

17th July 2017

What a difference a week makes. For the last two weeks central banks had been upsetting markets with their hawkish tone – but that all changed this week, sending equity markets higher.

In the UK, Ben Broadbent, the Bank of England’s (BoE) Deputy Governor, provided us with some crucial insight into how the central bank may vote in August, by saying that he is not ready to vote for higher UK interest rates. As I have said ad nauseam, although UK inflation is running ahead of the BoE’s target at 2.9%, this is predominately due to the pound’s sharp fall since the EU Referendum result last June (which makes imports more expensive) and as a result, I believe that an increase in UK interest rates would be a policy error as it would simply exacerbate the current consumer retrenchment (M&S this week reported weaker-than-expected Q1 sales).

In the US, the Fed Chair Janet Yellen, gave a two day congressional testimony this week. Although she played a pretty straight bat by sticking to the Fed’s outlook for gradually rising inflation and interest rates over the next few years, her testimony had a dovish tone as she signalled that the Fed doesn’t need to rush to tighten monetary policy as inflation is below their 2% target.

In addition to Janet Yellen, her colleagues Lael Brainard and Robert Kaplan also opined this week. Both indicated that they would prefer to see inflation moving toward the central bank’s target before removing accommodation.

And today’s (Friday 14 July 2017) US CPI inflation showed that prices continued to slow! June CPI was up only 1.6% year-over-year, down from 1.9% in May (the Fed has previously stated that the slowing US inflation was transitory – today’s reading implies that it isn’t).

I believe it is now pretty hard for the Fed to stay on their stated interest rate path (i.e. another interest rate increase this year followed by three rate increases in both 2018 and 2019) and that a December 2017 interest rate increase is looking doubtful, while the Fed’s plans to start reducing their balance sheet (reversing QE) must now also be in question for this year.

Economic highlights this week include UK and eurozone CPI and an ECB monetary policy meeting. Thankfully there are no Fed speakers this week as they are in blackout mode ahead of their next monetary policy meeting on 25-26 July 2017.

Ian Copelin, Investment Management Expert*

*Ian Copelin is an Investment Director at Wealth at Work Limited which is a member of the Wealth at Work group of companies

The latest market updates are brought to you by Investment Managers & Analysts at Wealth at Work Limited which is a member of the Wealth at Work group of companies.

Links to websites external to those of Wealth at Work Limited (also referred to here as 'we', 'us', 'our' 'ours') will usually contain some content that is not written by us and over which we have no authority and which we do not endorse. Any hyperlinks or references to third party websites are provided for your convenience only. Therefore please be aware that we do not accept responsibility for the content of any third party site(s) except content that is specifically attributed to us or our employees and where we are the authors of such content. Further, we accept no responsibility for any malicious codes (or their consequences) of external sites. Nor do we endorse any organisation or publication to which we link and make no representations about them.